We have written extensively on the US Securities and Exchange Commission (SEC) proposal to require that public companies disclose climate-related information and other environment, social, and corporate governance (ESG) trends. However, the European Union (EU) is at the vanguard of emerging requirements focused on climate-related information and broader ESG-aligned information.

Recent and forthcoming regulatory developments will have significant implications not just for EU-based companies but for those beyond, as well. Late last month, the European Parliament and Council of the EU announced they have reached political agreement to move forward with and expand applicability of a proposed measure that would require corporate sustainability reporting from a vastly increased number of companies. This change and others could have important impacts on businesses that merit close attention, including by non-EU companies. This post is meant to provide a quick primer on the EU’s array of trending ESG efforts and preview what additional requirements are expected in the future.

Backdrop of EU Sustainable Finance Framework

The EU ESG efforts dovetail with its mission to deliver on the European Green Deal, the aggressive, whole-economy approach to make Europe the first carbon neutral continent on the globe by 2050, and its intermediate goal of reducing greenhouse gas (GHG) emissions by at least 55 percent compared with 1990 levels by 2030, codified in the European Climate Law. The EU believes sustainable finance is a key component of its ability to achieve these targets. The “sustainable finance” framework encompasses a range of initiatives aimed at harnessing investment toward a clean economy, including:

- The Taxonomy Regulation establishes a classification system indicating which economic activities, across a wide range of industries, are environmentally sustainable. Whether an activity is identified as sustainable depends on whether it makes a “substantial contribution” and does “no significant harm” to a series of environmental objectives, as well as meet certain minimum social safeguards and technical screening criteria.

- The Sustainable Finance Disclosure Regulation (SFDR) imposes ESG disclosure requirements on financial market participants and products in the EU, aimed at protecting investors from greenwashing concerns.

- The Corporate Sustainability Reporting Directive (CSRD), a successor to and expansion of earlier corporate disclosure requirements, will require many large companies and companies with securities listed on EU-regulated markets to disclose a broad array of information under the E, S, and G pillars.

- The Green Bond Standard encourages the issuance of and investment in green bonds to help finance Europe’s low carbon transition by setting a voluntary standard for green bonds to ensure sustainability and investor protections.

- Benchmark labeling and ESG disclosure requirements serve to increase the ESG transparency of benchmark methodologies.

While all of these initiatives could be impactful to companies with European operations, here, we will focus in on the CSRD because of its far-reaching effects that will impact not just EU-based companies but certain US-based companies with operations in the EU and require significant planning to ensure adequate tracking, accounting, and reporting of requisite ESG information.

To whom will the CSRD apply?

Although corporate sustainability disclosure requirements are not new in the EU, the CSRD is a marked expansion. The Non-Financial Reporting Directive (NFRD), which has required certain companies to report for several years, currently applies to fewer than 12,000 large, “public interest” companies (i.e., listed companies, banks, and insurance companies). Under the CSRD, however, it is estimated that nearly 50,000 companies will have to report. That includes:

- all large companies (i.e., those meeting at least two of three criteria: more than 250 employees, greater than €40 million in turnover, and balance sheets above €20 million), whether they are listed on EU regulated markets or not;

- all listed companies (i.e., those offering securities on EU regulated markets), including small and medium-sized enterprises (SMEs) but excluding micro-undertakings (all of which are defined under the EU’s Accounting Directive 2013/34/EU); and

- non-European companies that generate a net turnover of €150 million or more in the EU and have at least one subsidiary or branch in the EU.

The first of these applicability criteria has the potential to draw in the EU subsidiaries of non-EU companies but the third criterion – which was added as part of the political agreement announced last month – makes certain the CSRD’s applicability to some non-EU based companies.

What does the CSRD require?

Subject companies will need to comply with European Sustainability Reporting Standards (ESRS), mandatory EU-wide ESG reporting standards, as well as with certain principles and audit and reporting format requirements.

- European Sustainability Reporting Standards (ESRS)

The standards are still under development by the European Financial Reporting Advisory Group (EFRAG). The initial set of proposed reporting standards are due to be released later this year, and adopted next summer, specifying disclosure requirements under ESG pillars on a “sector agnostic” basis. A further set of “sector specific” standards is due to follow after that.

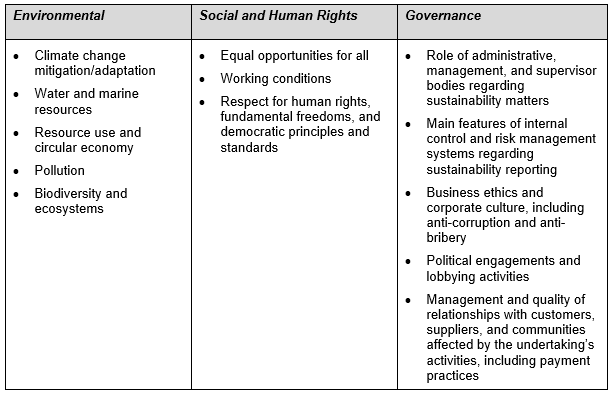

The EFRAG has issued a “roadmap” for development of the standards and a series of working papers, however, indicating the contents of at least some of the ESRS. Generally, the ESRS will require a myriad of disclosures falling within certain categories under each of the “E,” “S,” and “G” pillars, listed below:

Within each of these reporting standard areas, companies would need to make disclosures related to strategy (i.e., strategy and business model, governance and organization, impacts, risks, and opportunities), implementation (i.e., policies, targets, action plans, and resources), and performance measurement.

- Double Materiality

Because of these twin aims of informing both investors and the public, the CSRD is based on the principle of “double materiality” – meaning that companies need to disclose not just effects of ESG factors on its own operations (i.e., inward looking) but also their operations’ effects on sustainability goals (i.e., outward looking).

- Third Party Assurance

The CSRD proposal would also impose a third party assurance or audit requirement for sustainability information. At first, companies would need only provide “limited assurance.” Later, however, the proposal contemplates that a more rigorous “reasonable assurance” would be required.

- Reporting Format

Rather than releasing a separate “sustainability report,” the CSRD will require that all necessary disclosures are presented in a separate section within a company’s management report. The goal of this is to reinforce the importance of sustainability information and provide for consolidated financial and sustainability information. Also, for groups of related companies subject to the CSRD, a single, consolidated report can satisfy the reporting requirements. Additionally, the sustainability information will need to be digitally “tagged” to allow for the information to be fed into a single access point database.

Why the expansion of the CSRD?

A couple of motives are driving the CSRD. One is to ensure sustainability information is available to entities subject to SFDR requirements. The SFDR was adopted in 2019, and initial disclosure requirements are already in force, but requirements under the SFDR are evolving. This past spring, for example, the European Commission adopted a Delegated Regulation to supplement the SFDR and prescribe the specific content, methodology, and presentation of information to be disclosed. If agreed to by the European Parliament and the Council, the updated SFDR requirements would apply beginning starting next year. But financial market participants subject to the expanding SFDR requirements are finding themselves in a lurch in terms of available data to support their own reporting obligations. The CSRD’s reporting requirements will thus help to provide adequate corporate sustainability information for SFDR compliance.

Another factor is a desire to provide general stakeholders with sustainability information about companies with significant EU operations, which may drive consumer decisions or further policymaking.

Finally, part of the rationale for the addition of non-EU based companies with significant EU operations among the list of subject entities is to help level the playing field between the rigorous regulatory and reporting standards applicable to EU companies and the potentially more relaxed standards for companies based elsewhere.

When will CSRD obligations begin?

The CSRD is slated for final adoption late this year. EU member states would then need to translate the CSRD into their national laws within 18 months. Under the proposal, standards would become applicable first for companies already subject to the NFRD beginning in 2024, with initial reporting due in 2025 for the prior year. Applicability to the remaining subject entities would be staggered:

- Large undertakings would need to comply the following year in 2025 with the first report in 2026;

- SMEs would follow a year later, with applicability beginning in 2026, and reporting starting in 2027; and, finally,

- Non-EU companies covered by the CSRD would be subject starting in 2028, with the initial reporting due in 2029.

How should US companies prepare?

First, US companies should be aware that expanded ESG reporting is coming, and not just from the SEC or emerging state laws. Grasping now that your company may be subject to multiple ESG reporting frameworks is important to institute appropriate strategies to track and account for the information that will need to be gathered to satisfy divergent – or even conflicting – reporting standards.

Next, the CSRD requirements seem onerous – and they are – but, based on the proposal, there is a long lead time before initial reports will be due for non-EU companies subject to the CSRD. Moreover, large, EU-based companies will be required to report long before non-EU companies, and thus to road test the requirements. That should allow non-EU companies subject to the CSRD sufficient time to implement mechanisms to track the necessary information, but also to reap the benefit of others’ work in establishing best practices and experience.

Lastly, keep in mind that things are moving fast in the EU; not just in the ESG space but across the regulatory spectrum through implementation of the European Green Deal. If you have operations or otherwise do significant business in the EU, it is important to stay abreast of developments there that may affect you.